2026#08: Trump’s Tariff Twist: A Weekend Mood-Changer for Indian Equities

While structural breadth remains weak, the striking down of Trump's reciprocal tariffs offers a sentiment reset.

Indian equities ended the week with mild gains at the headline level but clear signs of fatigue as indices struggled with a major mid-week sell-off before staging a late recovery on Friday. Thursday was a bruising session, with indices plunging following geopolitical escalations in the Middle East. Breadth in the broader market stayed weak even though the indices still managed to end marginally in the green. However, the U.S. Supreme Court’s late-Friday ruling to strike down Trump’s reciprocal tariffs provides a major sentiment reset, replacing trade uncertainty.

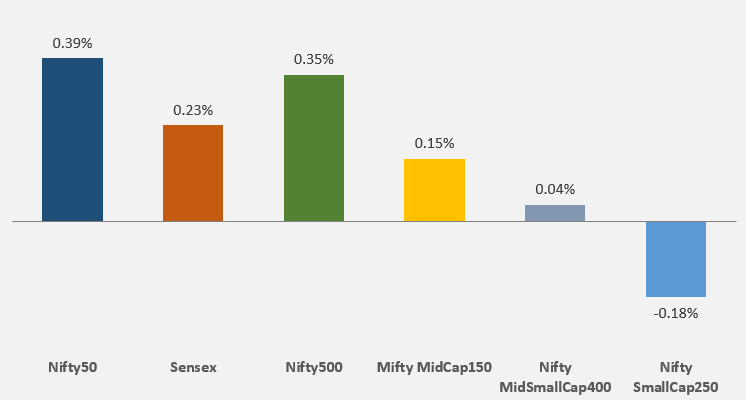

Key Indices Performance

Large caps outperformed this week, with Nifty50 and Sensex gaining 0.39% and 0.23% respectively, while small caps slipped a modest 0.18%.

Key Drivers for the Market

Trump Tariff Twist:

On February 20, 2026, the U.S. Supreme Court delivered a major blow to Trump’s trade agenda by striking down his sweeping global ‘reciprocal’ tariffs. The news came late after our markets closed the Friday session.

However, hours later, Trump signed a new executive order to impose a temporary 10% global tariff, which will be valid till 150 days, after which it requires Congress’ approval for extension.

Wall Street reacted positively. As far as India is concerned, uncertainty of tariff rates was removed to a large extent after reciprocal tariffs were brought down from 50% to 18%. Under the new 10% global tariff, India will face this rate for 150 days starting February 24. The market prefers a predictable small tax over an unpredictable huge tax. This will make the market optimistic for the weeks ahead.

Indian equities are likely to open higher on Monday in reaction to this update, though volatility is expected to continue. Any official notification on these new, lower rates will be the single largest driver for the Indian markets for a sustained run.

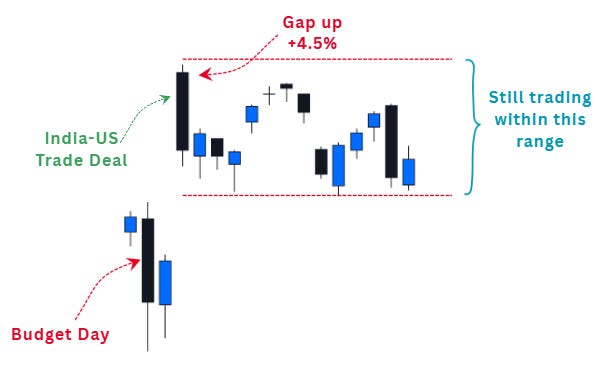

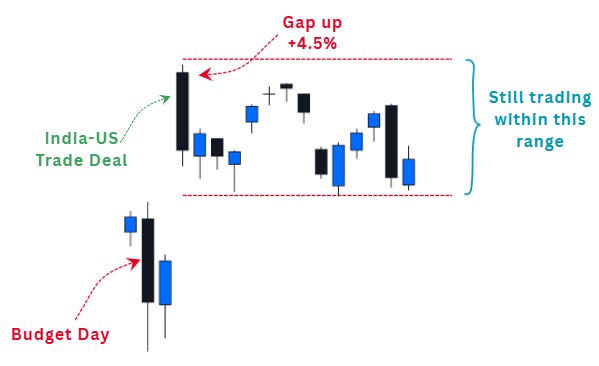

The 50% tariff on Indian goods was reduced to 18% following a trade deal announced on February 2, 2026. This policy change led to an immediate positive reaction in the Indian stock market. On February 3, 2026, the Nifty500 gapped up over 4.5%, however, only for half of those gains to vanish within days as the index failed to sustain higher levels till now. We do not want only a short-term spike because of this update.

Geopolitical Tensions: Escalating friction between the US and Iran was the primary catalyst for the Thursday crash. Any further updates regarding the conflict will be important to track.

Technical Perspective

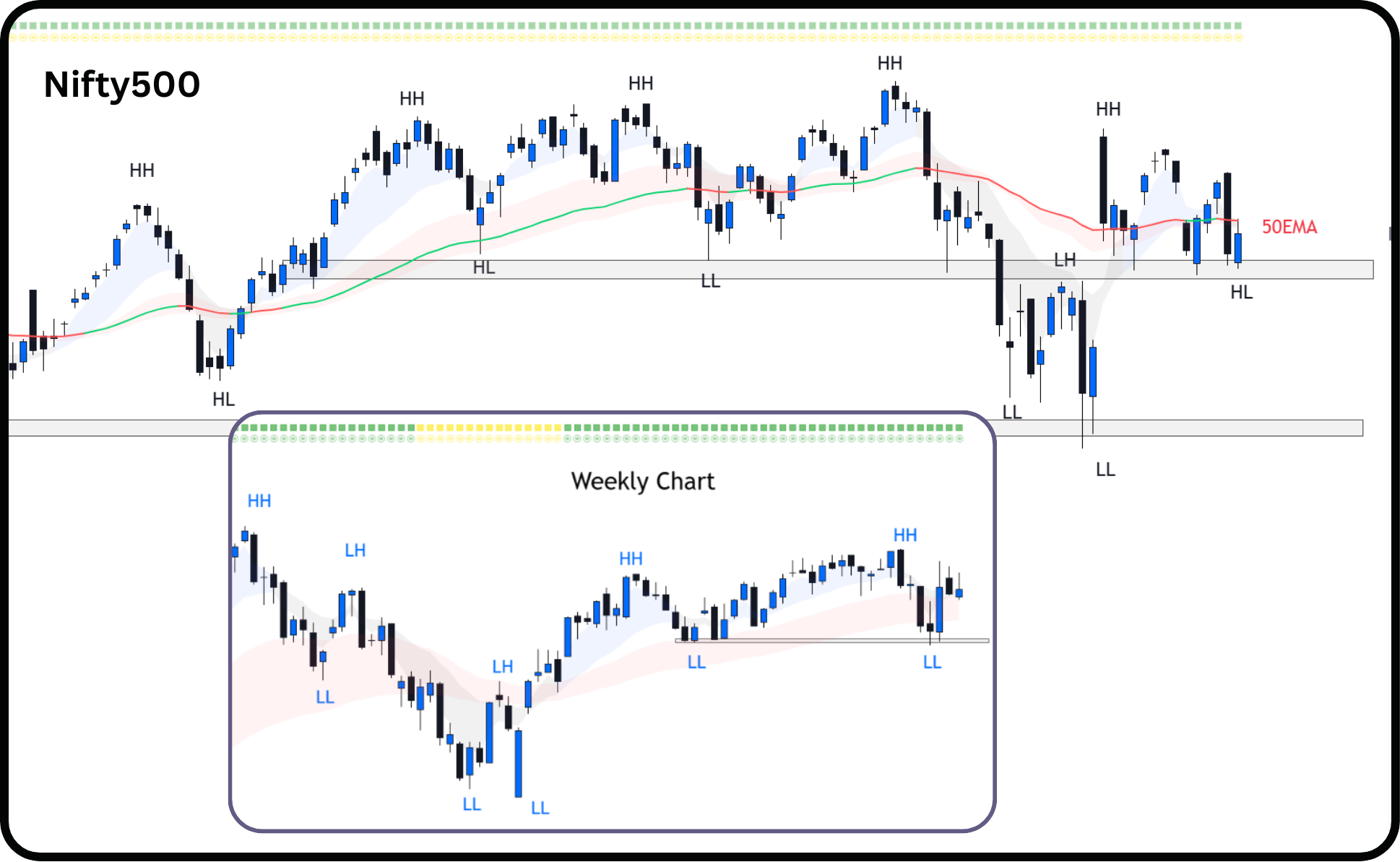

Nifty500 had gained roughly 1.4% till Wednesday, until Thursday’s crash erased all such gains. Friday’s recovery brought some relief.

Since the post-Budget recovery, the index has failed to form a new Higher High and is instead drifting back toward its recent swing lows.

On weekly chart, Nifty 500 continues to trade within a long-term consolidation range. There is a clear loss of upward momentum but not a full breakdown of the primary long-term trend.

50EMA: The index must cross and sustain above 50EMA level to signal a true shift from a relief rally to a sustainable uptrend as the first sign of recovery.

Critical Support Zone: The index took support from the 23,150-23,250 demand zone, as was identified in the previous week’s newsletter. Since this is a well respected zone, we adjust our drawing to reflect this zone.

The February 1 post-Budget low (around 22,300-22,400 levels) - a breach here would be technically catastrophic.

Nifty500’s 10EMA, 20EMA and 50EMA are currently converging indicating loss of immediate directional momentum.

The reason we track Nifty500 is because it represents over 90% of the free float market capitalization, making it a comprehensive barometer of market health.

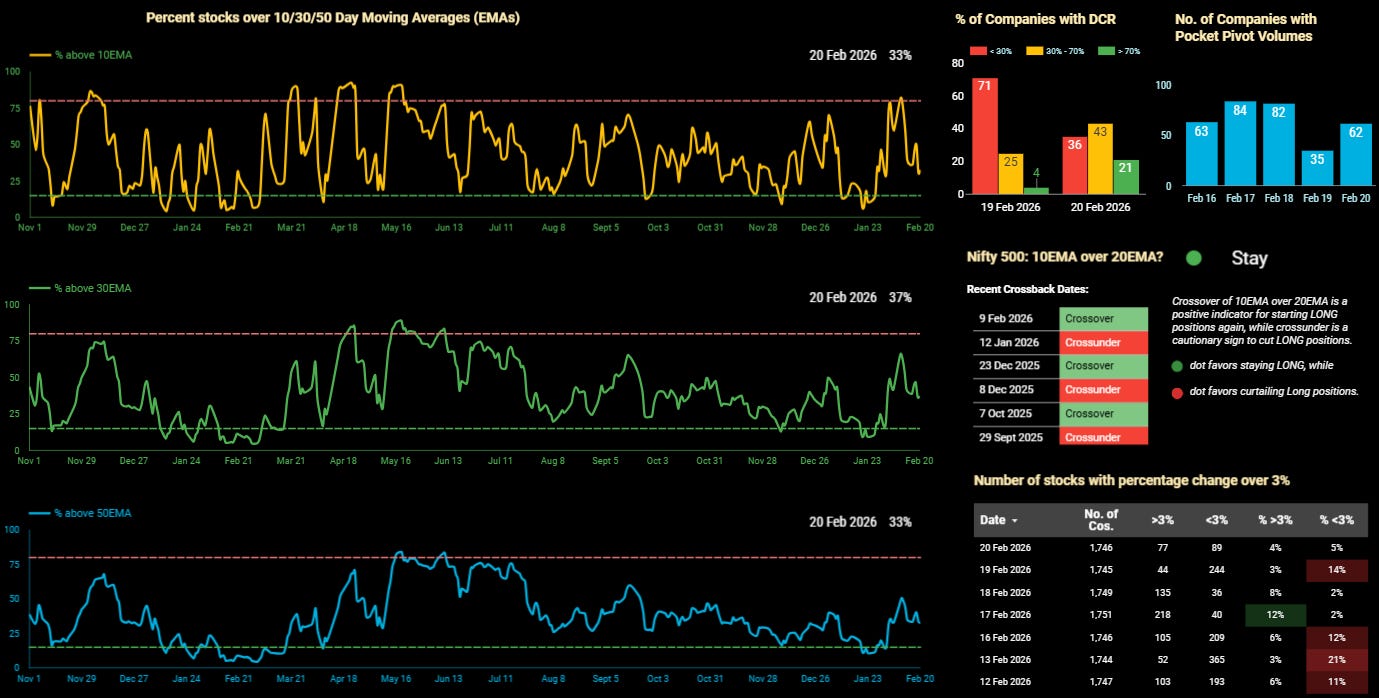

Nifty500’s 10EMA crossed above its 20EMA on 9th February triggering a ‘Stay’ signal that suggests maintaining long positions.

The market is currently experiencing a period of sideways consolidation with a cautious undertone.

Participation has continued to drift lower this week, indicating that individual stocks are struggling to maintain the momentum seen earlier in the month.

All three major breadth indicators are now clustered in the 33-37% range. This is well below the 50% ‘neutral’ mark, confirming that two-thirds of the Nifty500 stocks are currently trading below their short-to-medium-term trend lines.

10EMA: 33% of stocks are now trading above their 10EMA, compared to healthy 40% last week.

30EMA: 37% of stocks are above their 30EMA, compared to 42% last week.

50EMA: 33% of stocks are above their 50EMA, compared to 35% last week. The 50EMA breadth has stalled around the same level, failing to cross the critical 50% midpoint, which means that the broader market is still structurally weak.

It is important to note that overbought or oversold signals are most relevant for swing traders, as they reflect short-term momentum shifts.

Accessing Market Breadth on Pro-Setups Dashboard is available for all readers. Click on the link below.

Summary

Broader market breadth remained structurally weak with only 33-37% stocks trading above their key moving averages. However, sentiment is expected to shift following a late Friday U.S. Supreme Court ruling that struck down reciprocal tariffs. Although Nifty500 remains in a long-term consolidation range and closed just below its 50EMA, it is expected to have a positive reaction coming week. The primary concern for us is that these expected gains do not evaporate quickly, as seen previously. Although the significant reduction in tariffs is a welcome, trend-changing development, the market is now seeking a sustained run rather than a short-term spike.