2026#12: Oil, Rupee, and War: Markets on the Brink

As Brent crude surges past $110 and the Rupee hits ₹93.5, narrow leadership attempts a fragile bounce from oversold levels.

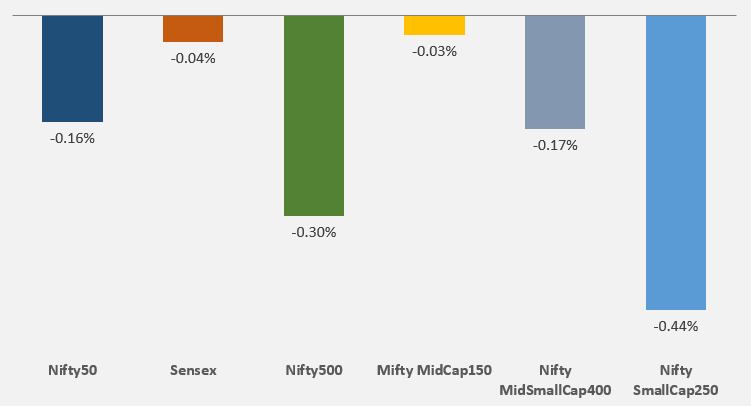

Last week had some signs of distribution beneath a range-bound index, with sharp selling early on and a lack of strong follow-through in the bounce. While the index held up, the market underneath became more selective, making it less favorable for broad-based trading setups

Key Indices Performance

Key Drivers for the Market

Geopolitical Escalation in West Asia: The primary catalyst for the market volatility and under-performance continue to be the intensification of the conflict in West Asia, involving Iran, Israel, and the United States. The fear of a wider regional war disrupted sentiment, leading to a visible lack of buying conviction even during dips. Any signs of de-escalation or, conversely, new sanctions or military movements will be the #1 driver for global markets.

Crude Oil Price Shock: Brent crude prices surged back above the $110/barrel mark due to fears of a supply crunch and the potential closure of the Strait of Hormuz. Higher oil prices directly hurt India’s import bill, a negative inflationary outlook, and eventual pressure on the corporate margins, amplifying the market’s downside reaction.

Rupee Volatility: The Indian Rupee plummeted to a fresh record low, crossing over ₹93.5/USD.

Technical Perspective

Establishment of Lower Low (LL): Nifty500’s recent price action has established a fresh Lower Low (LL).

Support Zone Broken: The Nifty500’s earlier support zone around 22,400-22,500 has been breached.

Death Cross: We made a death cross on Nifty500 last week. A death cross is a situation when 50EMA crosses under 200EMA, and it is considered negative in trading community. If history is to repeat again, then most market bottoms are formed within a couple of months of a death cross.

The reason we track Nifty500 is because it represents over 90% of the free float market capitalization, making it a comprehensive barometer of market health.

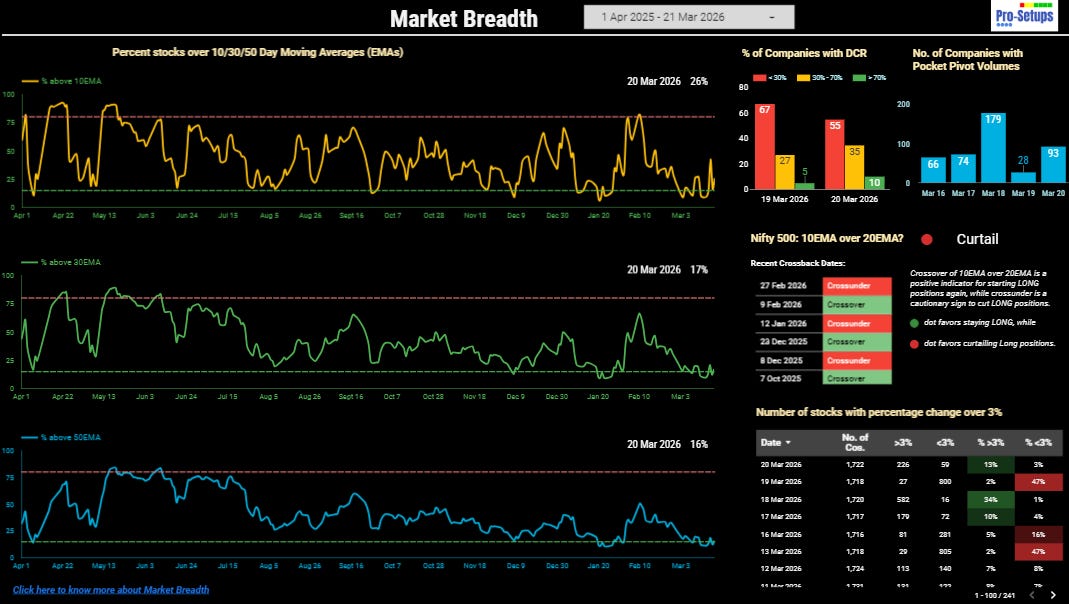

Breadth Comparison & Inference

The data suggests that while we have moved away from the capitulation lows seen last week - where all breadth metrics were sub-15% - the current bounce lacks broad-based participation. The minor uptick in short-term momentum is not yet reflected in the medium-term trend, indicating this may be a relief rally within a larger downtrend.

Strategic Interpretation:

Structural Health: Currently, only 16% of stocks are trading above their 50EMA. Since this is significantly below the 50% threshold, the market lacks structural strength. The dominant trend remains bearish, with the ‘Curtail’ signal on the Nifty500 (10EMA < 20EMA) confirming that selling pressure persists at higher levels.

Out of Oversold: Last week, the market was in a clear oversold zone as participation across the 10, 30, and 50EMAs fell below 15%. While we have technically moved out of that extreme oversold territory, the recovery remains shallow. The 30EMA participation sits at just 17%, confirming that the medium-term trend is still struggling to gain any real traction.

Execution Alpha: For the disciplined investor, the priority is to identify high-quality names with healthy valuation comfort (Valuation Grade A, A+, B and B+ in the Valuation Grade in the Pro-Setups Dashboard) that have maintained relative strength despite the broader index breakdown.

Accessing Market Breadth on Pro-Setups Dashboard is available for all readers. Click on the link below.

Summary

With less than 17% of the universe maintaining their 50EMA, There is an absence of broad-based participation. Currently, the recovery is driven by narrow leadership that also lacks the follow through. Hence, we are observing a fragile technical structure that is attempting a bounce from oversold levels, but without a significant expansion of participation above the 50EMA, the path of least resistance to the upside remains under pressure. Investors should remain cautious; until we see a meaningful crossover of the 10/20EMA and a surge in 50EMA participation, the bias remains titled to the downside.

The current outlook favors capital preservation and defensive positioning until key resistance levels and moving average crossovers are reclaimed.

| A guest post by

|