2026#18: The Small-Cap Party Continues While Large-Caps Tread Lightly

Navigating the US-Iran Tensions, Rupee Weakness, and the "Buy on Dips" Strategy

The Indian stock market witnessed outperformance by mid and small-caps while the benchmark indices (Nifty50 & Sensex) ended the week on a mildly positive note despite heightened volatility toward the close, driven by geopolitical tensions between the US & Iran and surging crude oil prices above $100 per barrel. Robust Q4 FY26 earnings in select pockets and aggressive retail buying in the mid-cap and small-cap segments kept the overall market breadth surprisingly buoyant.

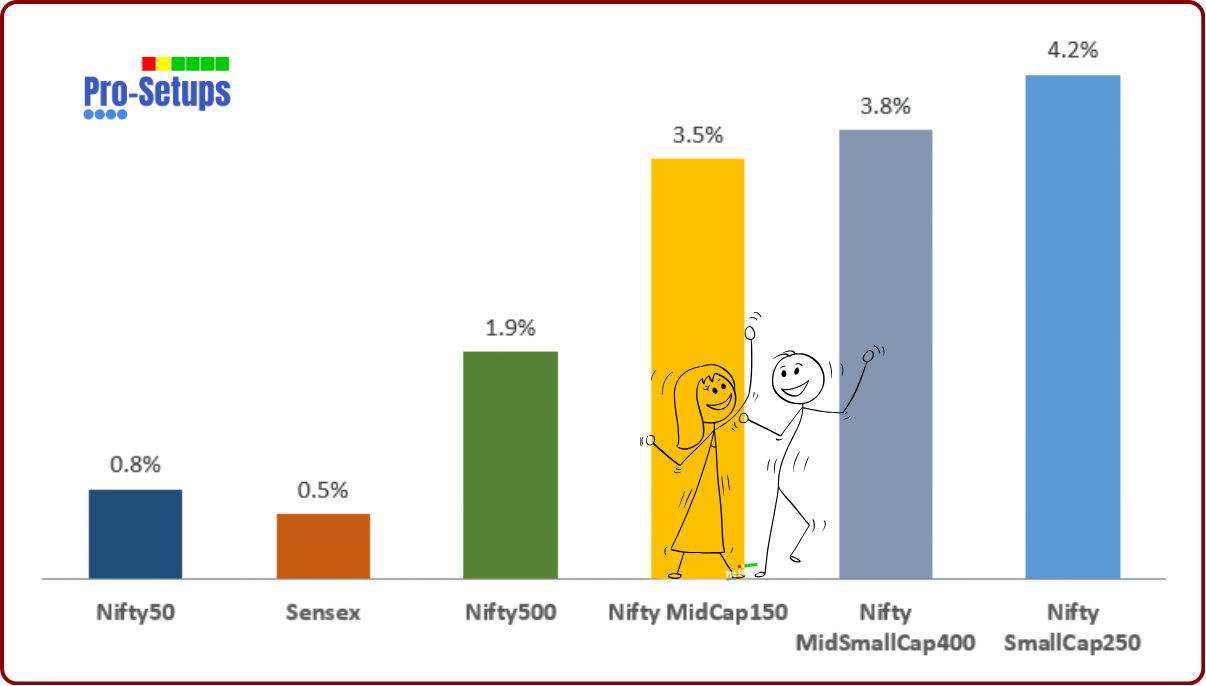

Large-cap stocks reflected narrow leadership, while the real party happened in the mid and small-cap space, which had broader participation and stronger conviction. Investors aggressively bought into the mid-cap and small-cap spaces. The Nifty500 advanced by 1.9% over the week, with small and mid-cap indices rising by over 3.5% each.

Key triggers in the week

Geopolitical Tensions Kept Markets on Edge: Escalation near the Strait of Hormuz triggered fears of supply disruption, pushing crude oil back above $100/barrel and weakening the Rupee toward ₹95/$.

Earnings Season Drove Market Leadership: Q4 FY26 results remained the key stock-specific trigger, with strong earnings and guidance sharply outperforming while misses saw aggressive selling pressure.

Domestic Flows Cushioned FII Selling: Continued DII buying helped absorb persistent FII outflows, supporting broader market resilience.

Crude and Rupee Remain Key Risks: Elevated oil prices and Rupee weakness continue to be the biggest macro headwinds, influencing inflation expectations, RBI policy outlook, and foreign investor sentiment.

Potential catalyst for the next week…

Will Crude Sustain Above the Panic Zone? Markets have already reacted to the initial oil spike. The focus now shifts to whether crude stabilizes or continues higher, which could materially alter market sentiment.

Can Nifty Hold Despite FII Pressure? Market resilience despite weak global cues would be an important sign of underlying strength. Traders should watch whether domestic liquidity continues to absorb foreign selling.

Broader Market vs Index Divergence: While index heavyweights remain under pressure, participation in midcaps and sector-specific pockets will be closely watched for signs of continued risk appetite.

Earnings Reactions Matter More Than Earnings: As the season progresses, management commentary, future guidance, and market reaction to results may become more important than the headline numbers themselves. After all, Good results may not be “good enough” if expectations are too high. Read why this matters in the blog below.

Bad Results? Stock Up! Good Results? Stock Down! What's Going On?

·

Most of us assume that if a company reports strong earnings and sales growth, its stock price will go up. After all, better financials mean the business is doing well, so why would not the market rew…

Technical Perspective

Nifty500 extended its recovery and continued to maintain a Higher High-Higher Low structure, signaling improving short-term trend strength.

Broad market participation remained healthy, with price sustaining above both the 20EMA and 50EMA after the recent rebound.

However, price is now approaching an important resistance zone from the previous consolidation area, which may lead to some near-term consolidation or profit booking.

With nearly 75-85% of Nifty500 stocks trading above their 10EMA, 30EMA, and 50EMA, market breadth continues to remain strong.

The 10EMA staying above the 20EMA favor a ‘buy on dips’ approach.

Pocket pivot activity remained elevated through the week, suggesting continued institutional accumulation and healthy momentum despite global macro concerns.

Short-term breadth, however, has cooled slightly from extremely overbought readings seen in late April, indicating the possibility of some consolidation, rotation, or stock-specific action rather than a straight-line rally next week.

Accessing Market Breadth on Pro-Setups Dashboard is available for all readers. Click on the link below.

Trading & Investment Strategy

The broader market structure remains constructive despite macro headwinds from crude oil, currency weakness, and FII selling. Traders should continue focusing on stock-specific opportunities driven by earnings, relative strength, and improving breadth. With market breadth still looking healthy, a “buy on dips” approach remains favorable, but position sizing and risk management become important as the market approaches key resistance zones and short-term overbought conditions.

Summary

Indian markets displayed notable resilience through the week, without any material damage to the market structure. Strong domestic liquidity, healthy market breadth, and continued momentum in select sectors indicate that risk appetite remains intact, although the next phase of the rally is likely to be more selective and earnings-driven rather than broad-based.