2026#28: Broader Market Steals the Show as Benchmarks Take a Breather

Mid and small-cap stocks outpace large-caps amid healthy risk appetite and resilient domestic liquidity.

Weekly Market Update: Week Ended July 10th, 2026

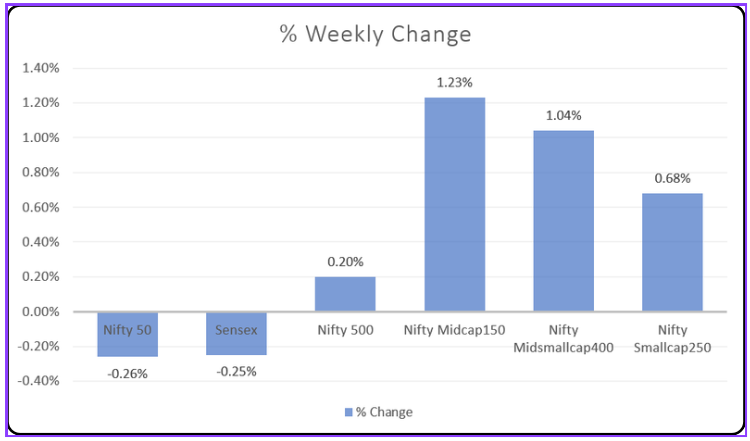

The broader market outperformed the benchmark indices this week, highlighting a continued shift towards higher-risk segments. While the Nifty50 and Sensex ended the week with marginal declines of 0.26% and 0.25% respectively, the Nifty500 managed to remain positive, gaining 0.20%. Buying interest was significantly stronger in the broader market, with the Nifty Midcap150 rising 1.23%, the Nifty MidSmallcap400 advancing 1.04%, and the Nifty Smallcap250 adding 0.68%. The clear divergence between the benchmark indices and the broader market suggests that investors continued to selectively accumulate mid- and small-cap stocks, reflecting healthy risk appetite despite the temporary weakness in large-cap names.

The week's divergence between large caps and the broader market was driven by continued stock-specific buying, healthy domestic liquidity, and sustained interest in the mid- and small-cap space despite profit booking in frontline stocks. In the coming week, market direction is likely to be influenced by the progress of the Q1FY27 earnings season and FII/DII flow trends which could determine whether the broader market's outperformance continues or broadens to large-cap stocks.

Technical Perspective

Nifty500 chart

Daily: The Nifty500 briefly registered a fresh Higher High, but the breakout failed to sustain as selling pressure emerged near the highs. Even so, the index continues to trade above its rising 50-day EMA, indicating that the recent decline is more likely a healthy pullback within an existing uptrend than the start of a larger reversal.

Weekly: The index is testing a crucial Lower High (LH) from the previous downtrend. A decisive close above this level would mark a significant improvement in the long-term market structure, confirming a transition from recovery to a sustained uptrend.

Outlook: The larger trend remains constructive, but the market is at an important inflection point. Holding above the recent breakout zone while overcoming the weekly resistance would reinforce the bullish case, whereas a break below support could extend the ongoing consolidation.

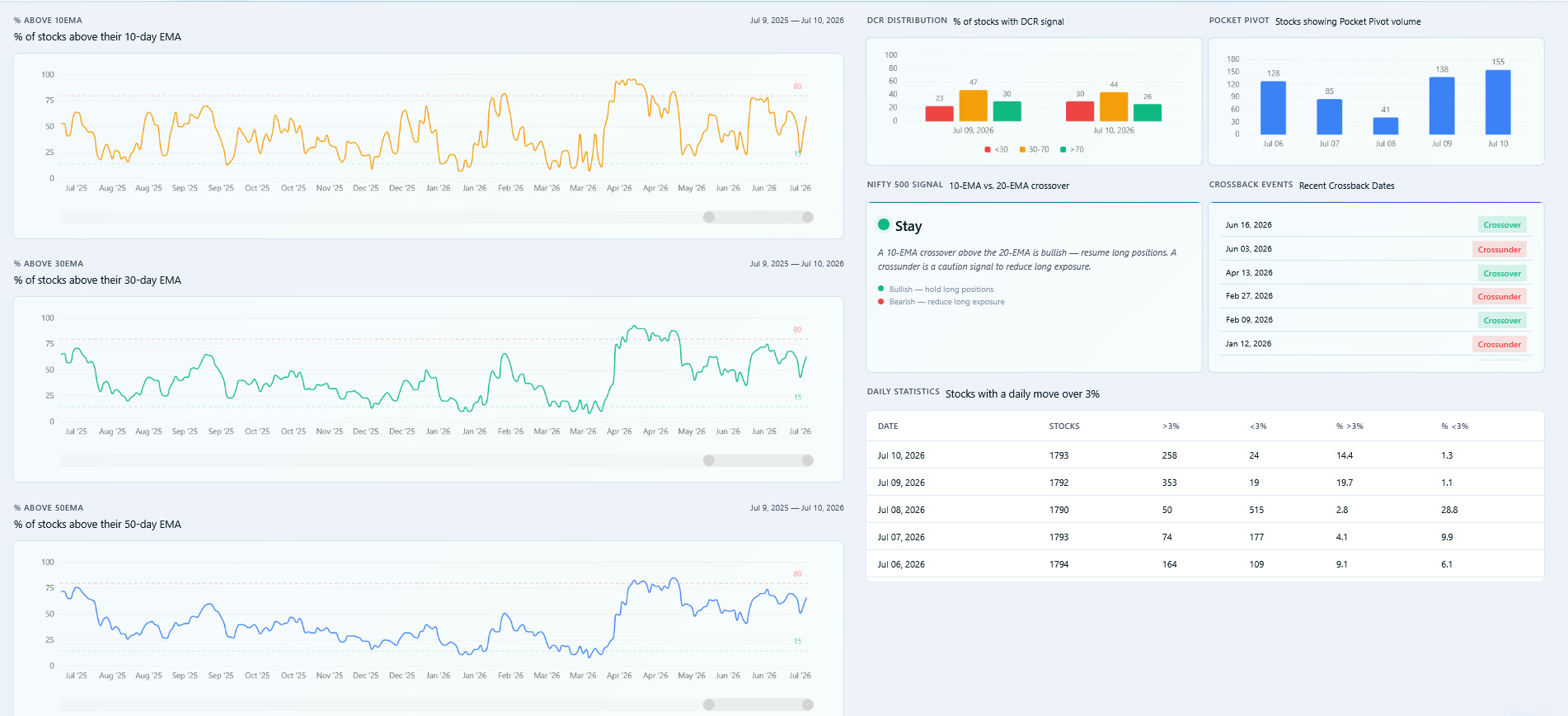

Market Breadth

The market's underlying breadth remained constructive throughout the week. While the percentage of stocks trading above their 10-day EMA eased to around 60%, indicating a pause in short-term momentum, nearly 60% and 55% of stocks continued to trade above their 30-day and 50-day EMAs, respectively, underscoring the resilience of the intermediate-term trend. This was further reinforced by the daily price distribution, where stocks advancing by more than 3% consistently outnumbered those declining by a similar magnitude, suggesting that the recent weakness reflects healthy sector rotation and consolidation rather than broad-based distribution.

The Nifty500 continues to maintain a bullish 10-EMA above 20-EMA, with the crossover that happened on 16th June, retaining the “Stay” signal. This indicates that the broader market remains in a positive trend, favoring existing long positions until a bearish crossover signals a change in market character.

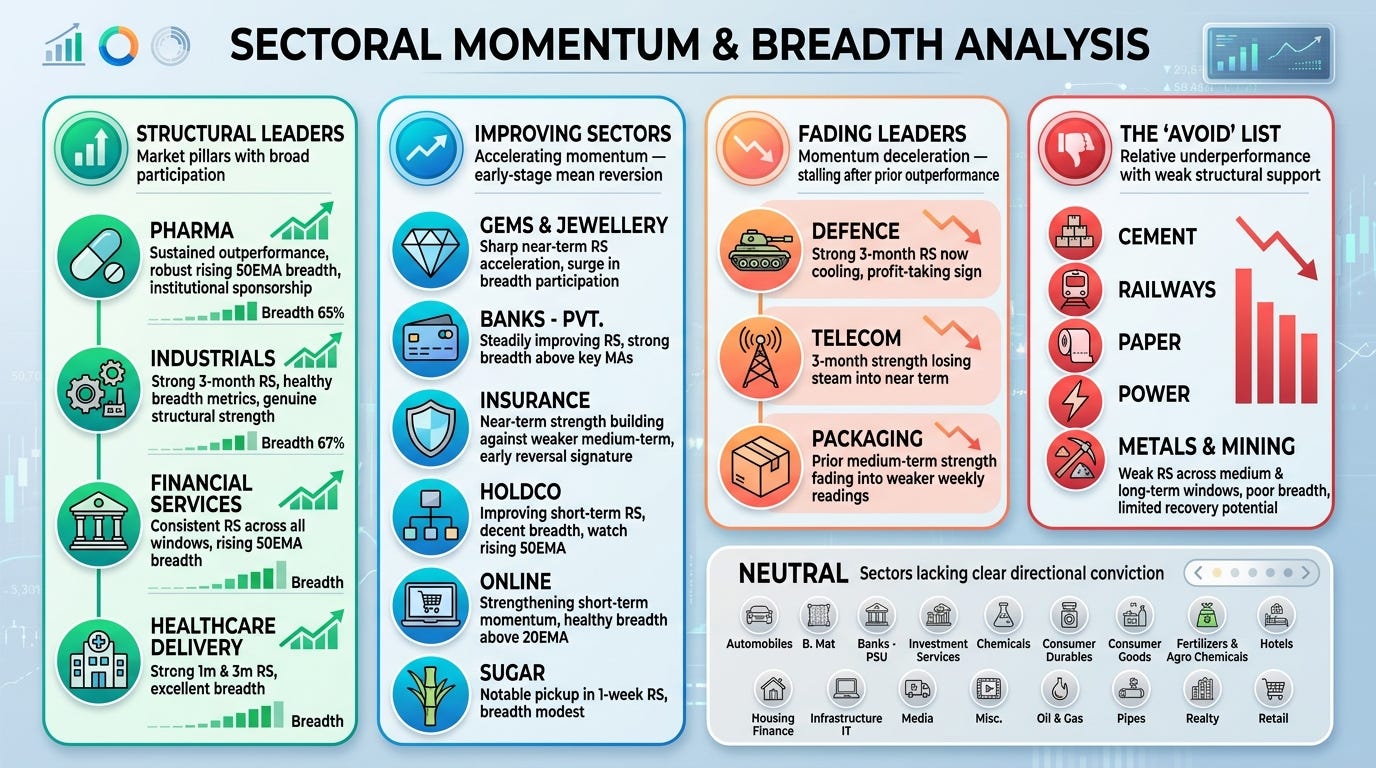

Sectoral Performance

Structural Leaders:

Pharma, Industrials, Financial Services and Healthcare Delivery continue to anchor market leadership, retaining strong relative strength across the 3-month, 1-month and 1-week timeframes, reflecting sustained institutional accumulation.

Emerging Leadership:

Gems & Jewellery, Banks - Pvt., Insurance, HoldCo, Online, Sugar have steadily improved their relative strength, signaling fresh buying interest.

Losing Momentum:

Defence, Telecom and Packaging have witnessed a noticeable decline in relative strength after outperforming over the past few months. Cement, Railways, Paper, Power, Metals & Mining continue to weaken, indicating that institutional capital is rotating away from these groups in favor of stronger themes.

Conclusion:

The sectoral landscape continues to favor a rotation-led bull market rather than a narrow rally. Leadership is broadening beyond traditional defensives, while persistent weakness is largely confined to a handful of sectors. Traders should continue to focus on stocks emerging from the Structural Leaders and Emerging Leadership groups, as these are most likely to offer the highest probability swing trading opportunities in the weeks ahead.

Trading Strategy for the Coming Week

The broader market continues to favor a selective, stock-specific approach rather than an index-led strategy. While the Nifty500 remains in an intermediate uptrend, the failed breakout and cooling short-term momentum suggest that traders should use pullbacks or confirmed breakouts as preferred entry opportunities and avoid chasing stocks that are extended.

Swing Traders: Focus on stocks exhibiting relative strength within the Structural Leaders and Emerging Leadership sectors. Give preference to stocks forming tight consolidations, pullbacks towards key moving averages, or early stage and fresh base breakouts backed by improving volume. Avoid lagging sectors, even if they appear optically cheap, as sector rotation continues to reward leadership over mean reversion.

Positional Traders: Continue to ride existing winners while maintaining disciplined risk management. The healthy market breadth and resilient intermediate-term trend support staying invested, but fresh allocations should be made selectively into stocks demonstrating strong relative strength and institutional accumulation.

Risk Management: The market remains in a “buy on dips” environment. As long as the Nifty500 holds above its recent support zone and the broader market breadth remains healthy, the bullish bias remains intact. A decisive breakout above the recent weekly swing high would provide confirmation to increase long exposure.

Summary

This week’s evidence can be distilled into three clear actionable messages:

Follow leadership, not laggards. Capital continues to rotate into sectors exhibiting persistent or improving relative strength.

Buy strength after confirmation or on constructive pullbacks. With daily momentum cooling, patience is likely to offer better risk-reward than chasing breakouts.

Stay invested, but stay selective. The weekly trend, breadth and sector rotation continue to support the broader bull market, even though short-term momentum has moderated.