2026#14: Seeking Value in a High-Volatile Environment

The broader market continues to lack structural strength. Yet a widening pool of stocks is emerging with low valuation comfort following the correction.

The Indian equity markets navigated a turbulent and volatile week, ultimately closing with modest losses, amid geopolitical tensions, elevated crude oil prices, and FII outflows. The week was marked by a dramatic mid-week slump triggered by escalating West Asia tensions and surging crude oil followed by a significant recovery during Thursday’s session.

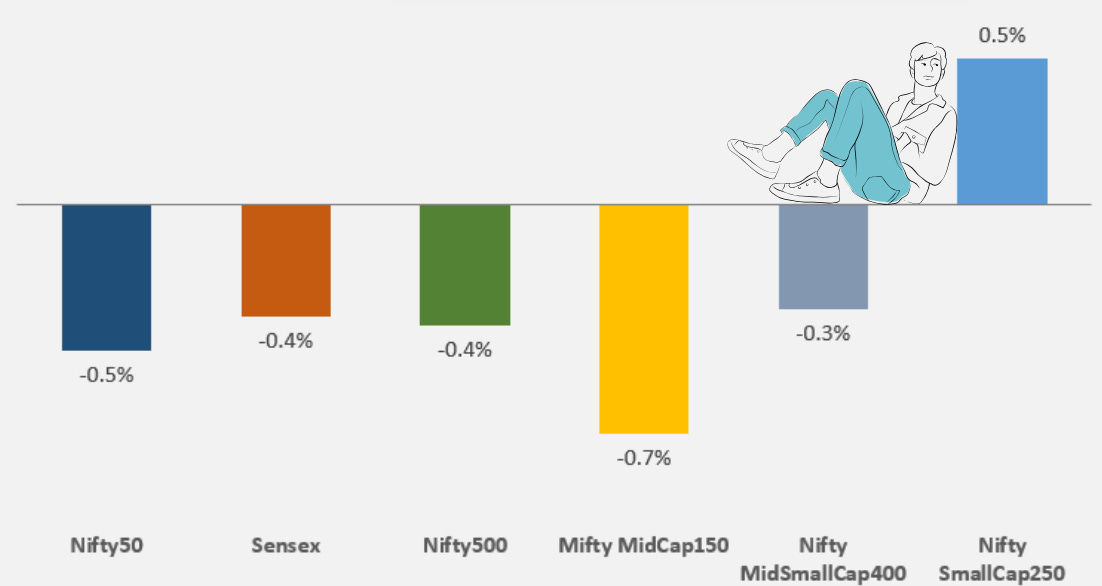

Key Indices Performance

The standout divergence came from Nifty SmallCap 250, that closed in the green at +0.5%, signaling selective buying interest in the small-cap space even as large and mid caps faced selling pressure.

With the recent correction, many small-cap stocks are now available at attractive valuations compared to their earlier premiums, making them increasingly appealing to investors looking to build positions at more reasonable entry points. To put this in perspective, there were 341 companies on March 4 that had a valuation grading of A and A+ combined. That list has soared to 454 companies on April 4 - a clear sign that the correction has opened up a wider pool of fundamentally sound stocks trading at compelling valuations.

Read more about our proprietary Valuation Grading score in the links mentioned below.

Key Drivers for the Market

Overall sentiment remained weak, with the Middle East conflict and sharp moves in energy prices keeping risk appetite in check. Major global markets, including the US and other developed economies, also ended the week on a mixed to negative note.

Geopolitical Escalation in West Asia: The ongoing US-Israel conflict with Iran, now in its fifth week, continued to escalate, keeping uncertainty elevated. Any further escalation or a potential de-escalation in the US-Iran conflict will remain the biggest driver for global oil prices and equity sentiment in the coming days.

Rupee Recovery & RBI Intervention: The Indian rupee staged a dramatic recovery this week, appreciating by over ₹2 to close at 92.67 driven by RBI’s strategic actions to curb speculation and volatility. This rupee strength provided a much-needed circuit breaker to the downside and triggered a sharp recovery in market on Thursday.

Crude Oil Price Shock: After falling to $97 per barrel this week, crude prices climbed back above $106 per barrel. For India, higher oil prices increase the import bill, push inflation higher, and put pressure on corporate margins leading to a negative impact on market sentiment.

RBI MPC Meeting (April 6-8): The Reserve Bank of India's first policy meeting of FY27 is the primary domestic trigger. Markets are closely watching RBI’s commentary for any shift in the neutral stance or guidance on liquidity management given the recent spike in crude-led inflation.

Corporate Earnings Season Kick-off: With the financial year coming to a close, focus now shifts to corporate earnings. Investors will closely track how companies performed in the last quarter of FY26 and how they factor in rising energy costs and currency weakness while giving guidance for FY27.

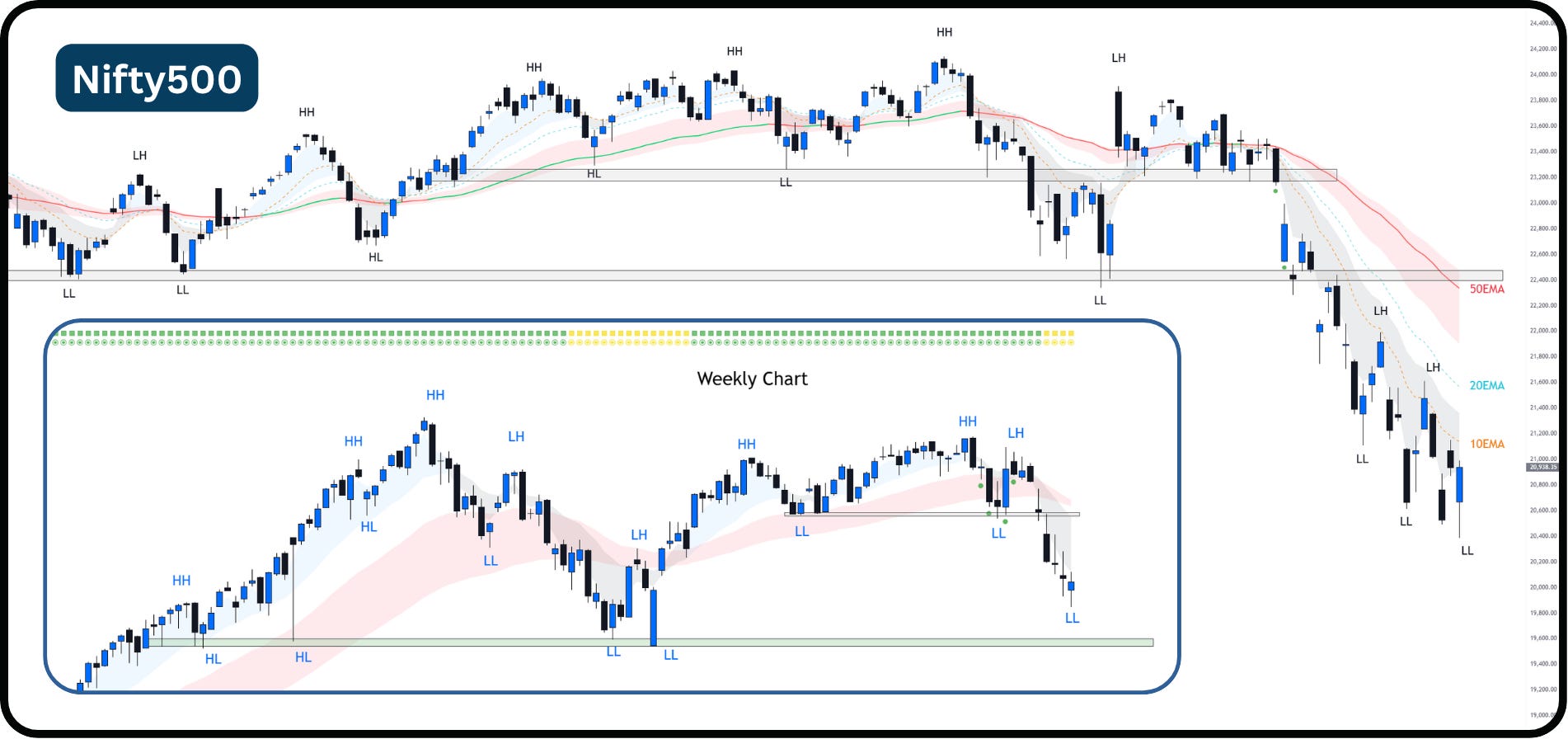

Technical Perspective

Establishment of Lower Low (LL): Nifty500’s recent price action has established a fresh Lower Low (LL).

Strong Resistance from 10EMA: The Nifty500 continues to show strong downward momentum, repeatedly facing resistance near the falling 10EMA..

The reason we track Nifty500 is because it represents over 90% of the free float market capitalization, making it a comprehensive barometer of market health.

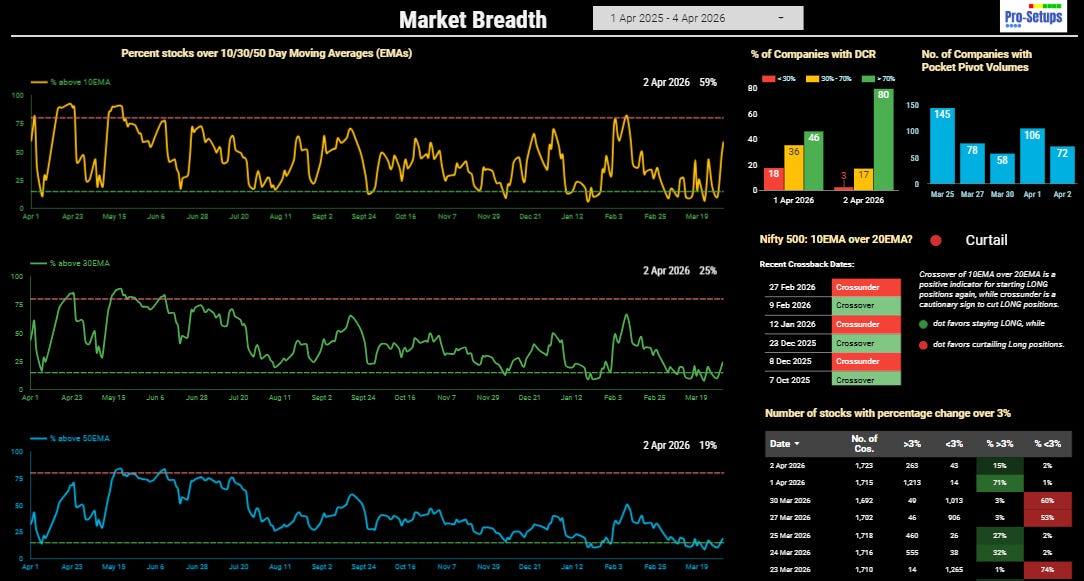

Breadth Comparison & Inference

The Nifty 500 is currently witnessing a notable momentum shift in short-term participation. At present, 59% of stocks are trading above their 10EMA, a sharp climb over the 19% seen a week ago on March 28. This surge suggests an early improvement in market sentiment, where stocks are beginning to reclaim near-term levels even as the index price remains lower than its previous weekly close. The medium-term health is also showing signs of life, with 30EMA participation rising to 25%, compared to 14% last week. This indicates that while the broader trend has been under pressure, a recovery is attempting to take root from the bottom up.

Structural Health and Technical Inferences

When analyzing the deeper framework, the market continues to exhibit a fragile structure. Currently, only 19% stocks are trading above their 50EMA. Based on quantitative benchmarks, because this figure remains significantly below 50%, the market fundamentally lacks structural strength. This disparity between short-term momentum (59% above 10EMA) and long-term health (19% above 50EMA) indicates that the recent recovery is likely driven by tactical mean-reversion rather than broad-based institutional accumulation. Since participation levels across the 10, 30, and 50-day EMAs are no longer all below 15%, the index is no longer classified in a potential oversold zone.

Summary of Nifty500 Performance

The Nifty500 ended the week at 20,938, a 0.4% decline from previous week’s 21,020. While we see a clear breadth expansion in short-term indicators, the “Curtail” signal on the index’s 10EMA vs 20EMA crossover serves as a lack of confirmation for a primary trend reversal. In essence, we are seeing a gradual improvement in daily participation, but the underlying weakness in the 50EMA suggests the broader trend remains cautious. For this move to be sustainable, we require a strong follow-through that pushes more stocks back above their long-term averages.

Accessing Market Breadth on Pro-Setups Dashboard is available for all readers. Click on the link below.

Execution Alpha: For the disciplined investor, the priority is to identify high-quality names with healthy valuation comfort (Valuation Grade A+, A and B+ in the Pro-Setups Dashboard) that have maintained relative strength despite the broader index breakdown.

Summary

While short-term breadth indicators are showing signs of improvement, the broader market structure remains fragile with the index still lacking structural strength. That said, there is a degree of softness in the bearish narrative as the market appears to be attempting a rise from the bottom up. However, for this recovery to gain credibility, Nifty500 must first navigate a series of overhead hurdles - the immediate resistance lies at the declining 10EMA, followed by the 20EMA and 50EMA, each of which needs to be reclaimed convincingly.

Until these key moving averages are cleared and we see a meaningful expansion in 50EMA participation, the bias remains cautiously defensive. Investors should stay selective, focusing on high-quality names with strong valuation comfort while allowing the market to prove its intent through sustained follow-through.